💳 The Magic Number: Why Limiting Your Credit Cards is Key to a High Credit Score

🎥 Watch Rob’s full breakdown on YouTube: 👉 Click here to watch

When “More” Hurts Your Score

One of the most common misconceptions about credit is that having more credit cards automatically helps your credit score.

After all, more credit means more available money, right?

Not exactly.

In a recent video, Rob Taylor shared a story about a client who had 32 credit cards — all paid on time — yet still struggled with a terrible credit score.

This client was shocked. “How can my credit be bad if I’ve never missed a payment?”

The answer comes down to how credit scoring models interpret risk.

Even if every payment is on time, having too many open accounts can make you look financially overextended — someone who could easily fall into debt if they decided to use all that available credit at once.

Why Fewer Cards = Higher Scores

The key takeaway?

You don’t need a wallet full of cards to prove you’re financially responsible.

Rob recommends keeping two to three major credit cards — that’s your magic number.

Here’s why it matters:

-

1️⃣ Simplicity reduces risk. The fewer accounts you manage, the less likely you are to miss a due date or lose track of balances.

-

2️⃣ Credit history looks cleaner. Scoring algorithms prefer long-standing, well-managed accounts over lots of new or short-term ones.

-

3️⃣ Lenders prefer consistency. Mortgage underwriters want to see stability, not constant opening and closing of lines of credit.

Having too many cards can actually make your credit profile appear unstable, even if you’re diligent.

The Hidden Dangers of Store Cards

We’ve all been there — you’re checking out, and the cashier says,

“Would you like to open a store card and save 20% today?”

Tempting, right?

The problem is that store cards often come with low limits and high interest rates, which can wreak havoc on your credit utilization ratio.

For example, if you have a $500 limit and charge $200, you’re already using 40% of your available credit — well above the ideal 25% threshold.

Even worse, each store card application triggers a hard inquiry on your credit report, which can temporarily lower your score.

So while those sign-up discounts might save you a few dollars in the moment, the long-term cost to your credit health isn’t worth it.

How This Impacts Homeownership

When you apply for a mortgage, lenders don’t just look at your score — they analyze your entire credit profile.

A high number of revolving accounts can raise red flags, signaling that you may be too reliant on credit.

Even if your payment history is flawless, too many cards can:

-

Increase your debt-to-credit ratio,

-

Lower your average account age, and

-

Make your overall credit picture look riskier.

By simplifying your accounts, you project financial discipline — something lenders love to see.

It can mean the difference between getting approved with a great rate or paying thousands more over the life of your loan.

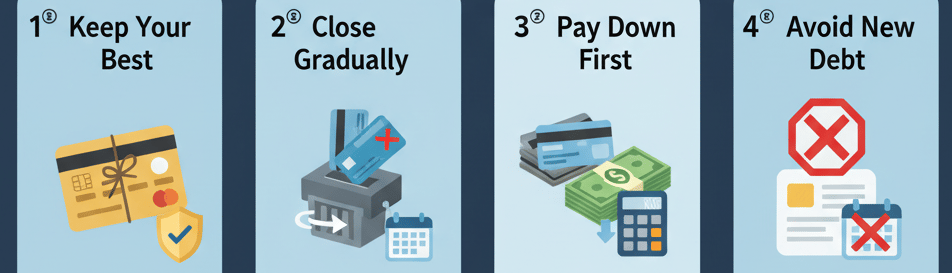

How to Simplify Without Hurting Your Score

If you currently have a dozen cards (or more), don’t panic — you can streamline strategically.

Here’s Rob’s recommended approach:

1️⃣ Keep your oldest, best-managed cards.

These help maintain a long credit history and strong payment record.

2️⃣ Close high-interest or low-limit cards gradually.

Don’t close everything at once — that can shorten your credit history and temporarily drop your score.

3️⃣ Pay down balances before closing accounts.

This ensures you aren’t increasing your utilization when you lose that available credit.

4️⃣ Avoid applying for new cards.

Every inquiry counts, especially if you’re planning to buy a home within the next year.

A Real Example from Team Taylor

Rob recently worked with a client who had 12 active cards.

After closing a few store accounts and paying down balances, their score jumped over 60 points in just three months — enough to qualify for a lower mortgage rate.

That’s thousands of dollars in savings over time, all by understanding how credit behavior affects lending decisions.

Final Takeaway: Keep It Simple, Keep It Smart

The goal isn’t to have no credit, but to have smart credit.

Two to three cards, managed well, can demonstrate strong financial control without the risk signals that come from juggling too many accounts.

Whether you’re trying to rebuild your credit or preparing for your first home purchase, simplifying your credit profile can be one of the fastest ways to boost your score — and your confidence — as a buyer.

Stay Connected with Team Taylor

💬 Need help getting mortgage-ready?

Team Taylor partners with trusted credit professionals who can guide you through every step of your financial journey — from improving your credit to closing on your dream home.

📱 Follow for more real estate and financial tips:

📺 YouTube: @teamtayloratkellerwilliams5814

📘 Facebook: Robert L. Taylor Realtor

📸 Instagram: @robsoldmyhouse